Today I will be reviewing 4 Digital lending apps or loan Apps that I have used. Most of the apps I will be mentioning here operate in the Kenyan marketplace.

Disclaimer: I am writing this article based on my experiences with loan apps. None of the information shared here is sponsored by any of the apps mentioned here . So, this article is solely to educate and inform the public . Use your own judgment when deciding on which loan app to download and borrow from.

How People Finds Themselves Taking Loans from Mobile Apps

People have different stories on how they got to know about loan apps. Many are like me; they were in a financial distress, and they were looking for a quick fix after all their friends failed to help. They then decided to search for answers on Google. Google then redirected them to GooglePlay store where they found the solution.

But at what price does this solution come with?

Since loan apps have been in existence long enough, nearly all tech savy people have an idea of how they work. Some apps have evolved to suite current customers needs while others; well, are yet to be hit by the reality.

One crucial thing that many people forget to look at when they are in financial distress is the details they give out in exchange for a loan.

That’s why I am here to take you through some things I have learnt after using digital loan apps.

Popular Keywords Used On Playstore

Loan Apps, digital lenders, instant loan, Quick loan. Searching using one of these keywords will display several loan applications. With more than 50 Apps showing up, that’s a lot of Credit at Hand if you think about it.

How you make you choices from here matters.

How much time do you have with you to decide on the app to take loan with? In my opinion, don’t rush. Take your time. Spend a day at least to look through these apps.

In this review, I will focus on the App UI design, Customer Data Collected, Profile Review time, Loan Processing Duration, Repay Time Frame, Fees and Customer Service.

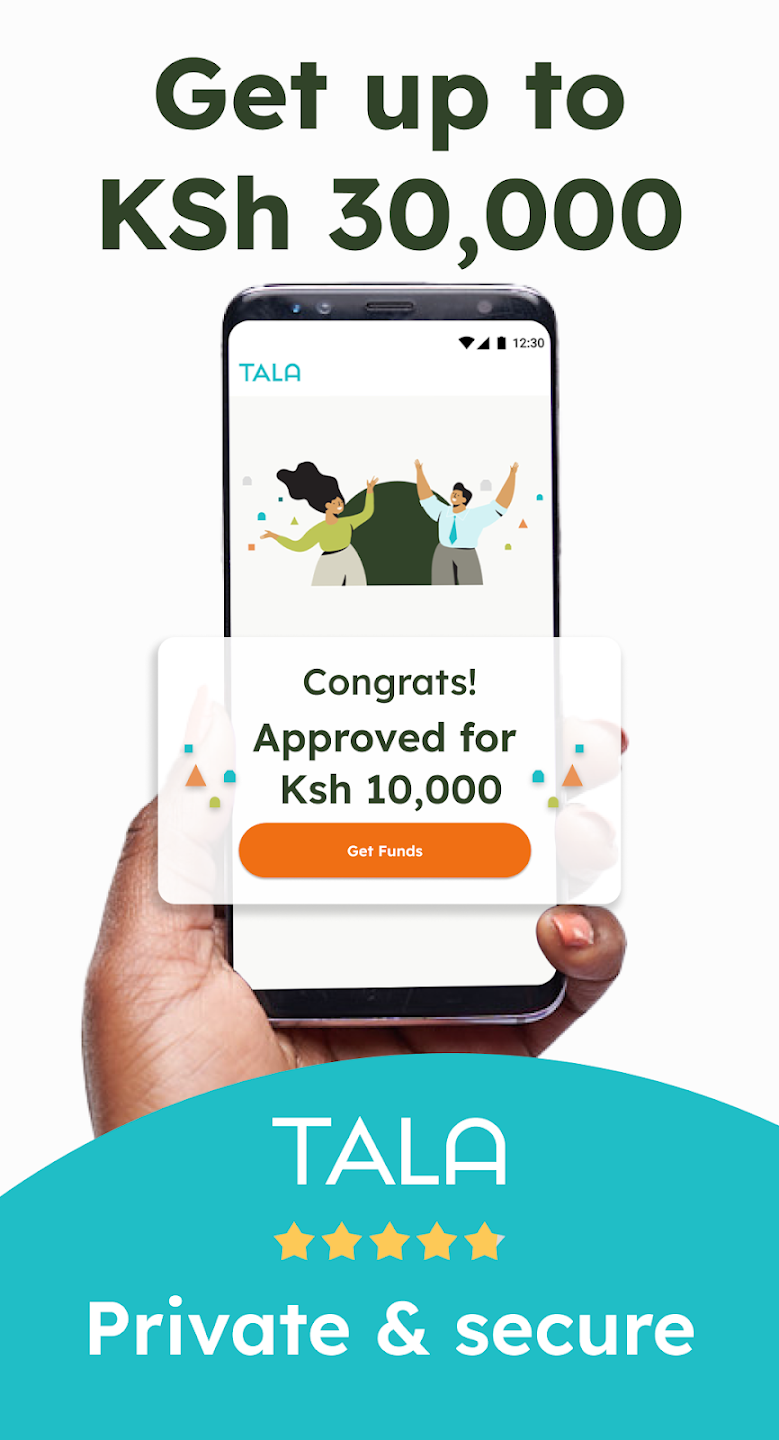

Tala Loan App

Tala loan app has been there since the year 2011. I first learnt about the app in the year 2014 from billboards but had never used it to borrow a loan. Two months ago, I was propelled to try it out after the long electioneering period. So here are my thoughts so far after using the app.

App UI– App UI looks good and polished. What you see displayed as screenshots from the app on PlayStore is how the app looks like after signing up.

Loan Application Process– This is where I felt a bit uneasy. More personal and business related data is required for eligibility. Also, the lender is interested to know how much money you make in a month and the frequency in which you receive the payment.

They also want to have your National ID number. This is a lot of private data if you think about it. So you have a choice to tell the truth or lie.

Another downside about the information you provide is; once you share the data, you are not able to access them again on the app via your profile.

Loan Application Time and Interest Rates – When making my first loan application it took less than 5 minutes for it to be approved. I was given a starting loan limit of Ksh.3,000 which on request, I received instantly on my Mpesa. So in terms of application review and loan approval, they are excellent. Their interest rate is at 0.3-0.6 % daily which is not bad compared to others when it comes to transparency.

Customer Service And Credit Collection– In terms of customer service, they are also above average. I was called once by their customer representatives reminding me to pay the loan on time so that my limit would increase. Other than that, I regularly received well drafted SMS reminders.

Repayment Deadlines – While I borrowed the loan for 30 days, I had up to 60 days to repay back. No penalty was imposed on the loan I borrowed.

Overall, this is a good app for anyone to borrow short term loans so long as they repay back on time.

Branch App

Branch was launched around 2015. Unlike other mobile lending apps, branch does more than offering loan to users. Users can save, pay bills and manage their finances on the go.

App UI Design– Branch has excellent app UI design. What you see on playStore is what you get when you sign up.

Loan Application Process – The process of applying for a loan is simple once you sign up with your phone number. You cannot apply for any loan unless you grant the app permissions to see installed apps on your phone, contacts, SMS and location. This is normal for most loan apps to secure your account once you login.

When applying for your first loan, you are required to confirm how much you earn in a month. Also, you need to take a selfie and upload it as part of the evaluation process.

Loan Application time and Interest rates – From the time I downloaded the app to the time I received the first loan, it took me 20 minutes. This is quite fast for a loan of Ksh.3400 considering I don’t have history with them. Their interest rate for 61 days is 35%. That’s about 17.5% per month. This is high compared to Mshwari loan whose charge is 8.5%. So the interest is on the downside.

Additionally, Branch charges transactional fees to withdraw the money from the app to Mpesa.

Customer Service and Credit Collection – Compared to Tala, branch credit collectors are a bit aggressive. They will call you once your first installment is due. They claim to use this to calculate the amount of credit you will receive next. Also they will encourage you to repay on time to qualify for a higher loan limit. In a month they called me and sent me 3 messages which was detected as spam on my phone.

Repayment deadline – You have to choose a period starting from 30 days. If you choose 60 days, they will request that you repay them back in two installments of 50/50 after every 30 days. They insist on this, something, which doesn’t go well when you haven’t gotten the funds to repay.

Overall, this is not a bad app for borrowing emergency loan going by the fact that they will charge you 17.5% interest on initial loans.

Truepesa

TruePesa promises to give people instant loans. That is true, but not that fast. You have to first have the app on your phone for 2 weeks before they give you the first loan. Secondly, the loan duration they promise in the description area on Playstore is not practical. I will be getting to that in a minute.

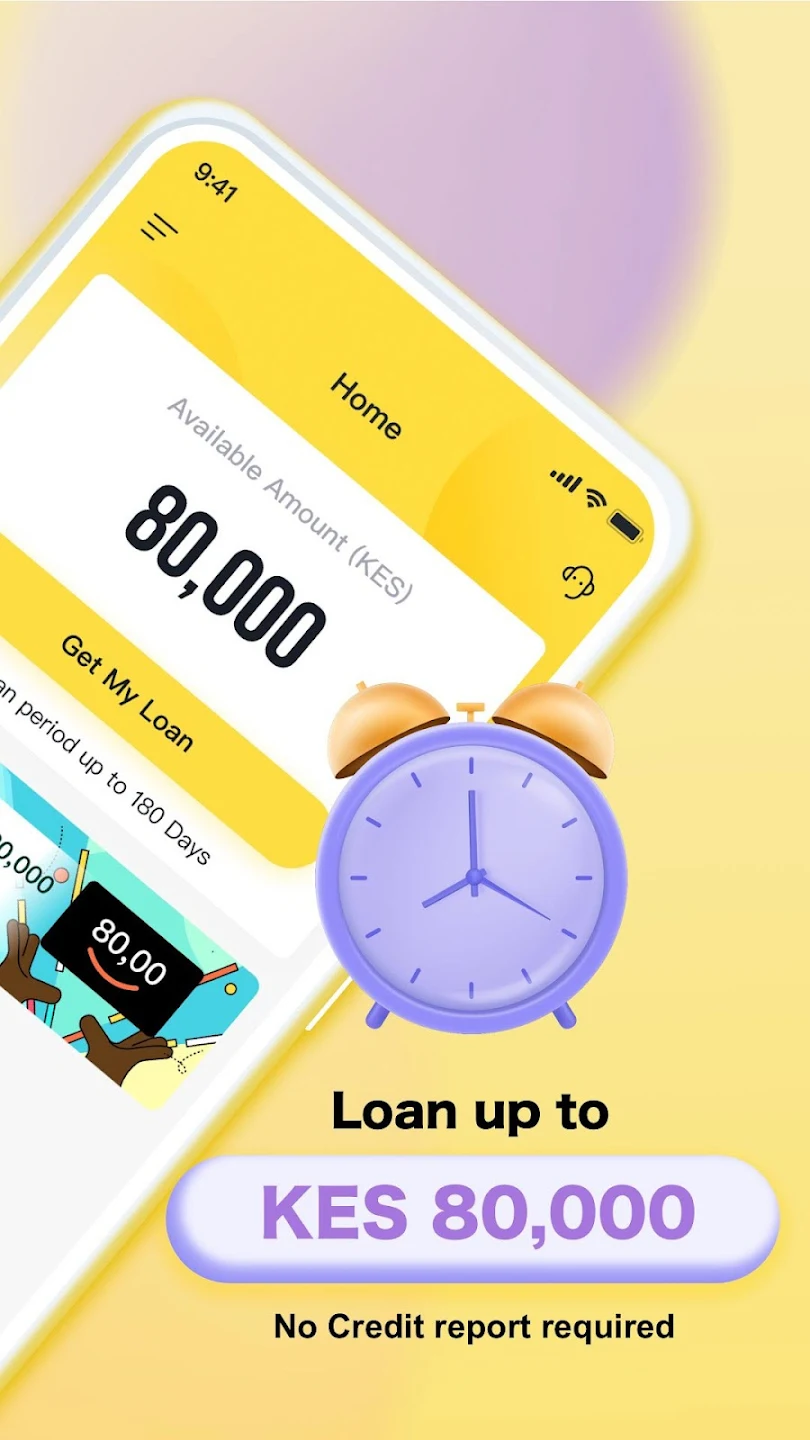

App UI Design – The app UI Design is clean. One thing you will quickly note with this app is, the UI design resemble the many loan apps on Playstore where once you install, there is a slider on the launch screen with a question; How much loan do you want? For Truepesa, the slider starts at Ksh.80,000. This is mouth watering to one in dire financial need.

So if you choose that you want Ksh. 80,000, will you get that amount? Let’s find out.

Loan Application process – You are required to sign up with your phone number and create a secret pin. Before your do this, the app requests for permissions on your phone which includes SMS, contact list, installed apps, external storage and phone location.

I feel this is too much considering you are taking your first credit. After you agree, it’s followed by the privacy policy. It’s important to read and understand what you are agreeing to.

Once you agree you will be signed up. This is where the show begins.

Loan Application Time and Interest Rates – When you sign up, they ask you few questions when applying the loan like what you do and your national ID number. After you complete the application, you will not get the loan. They want you to remain with the app installed on your phone for 2 weeks and they will be able to give you a loan.

Imagine remaining with an app on your phone that you have granted many permissions. Very risky.

On the other hand, if you were looking for an instant loan, this will be a big disappointment.

I uninstalled and installed the app 2 weeks later and I still had to wait for 2 days with the app installed on my phone for them to set a loan limit.

They have a weird credit disbursement process. For instance, if you request a loan of Ksh. 2,500, you will receive Ksh. 1,800. They will deduct their interest rates of 24% a week and send you the balance. This is 3 times what Mshwari charges their customers for 30 days.

Moreover, their loan period is 8 days and not 61 days they promise on Playstore.

Customer Service and Credit Collection – This guys will not contact you until the 7th day -a day to loan expiry. That’s when you will receive several scary messages like the one below.

3 days later, I had over 40 similar messages on SMS and WhatsApp. This to me is very unprofessional. That’s aside calling me more than 3 times a day using different numbers to ask me to repay their loan. Not everyone falls in this category to be intimidated. Am sure this app will only attract crooked customers who tolerates such communication manners.

Repayment deadline – They do opposite of what they promise on Googleplay. They tell you their loan tenure is 90-365 days with APR of 14-33%. You will be in for a shock when you sign up and wait for 2 weeks. That’s the rates they will charge you in 7 days. That’s a breach of contract. Not forgetting the amount of private information they have collected from you.

Overall, this is an app I wouldn’t recommend to anyone who is looking for a quick loan. That’s unless you are ready to be embarrassed and overcharged.

Zenka

I first learnt about Zenka loan app at the height of Covid-19 in the year 2020 . There was a video campaign on most social medias advertising the app.

They promise to give you loan for a period of 61 days to 1 year.

App UI Design – The app UI is clean and sleek. They use unique fonts in their app as well. The screenshots you see on Playstore is exactly how the app looks like when you download and sign up.

Loan Application process – The process of applying for a loan with Zenka is easy. You only sign up and share your national ID number and phone. Next, you fill in a questionnaire before you are allocated a loan limit, a process which takes 5 minutes.

Loan Application Time and Interest Rates – From downloading the app all through to loan approval and depositing to my Mpesa took me around 15 minutes.

I was allocated a loan limit of Ksh.3,000 on the first loan I applied with zero interest rate for 61 days.

This is an offer that none of the lenders on Googleplay does. Am yet to see the practicality of their APR interest they promise of 170-224%.

Customer Service and Credit Collection– Since I I took the loan, I have received only one marketing message from them. Compared to others, this is one of the peaceful loan I have taken from an app.

Who knows, maybe I will begin to see their true colours once the loan deadlines approaches.

Repayment Deadline – The deadline to repay the loan is from 61 days to 1 year. This a good time for anyone to look for money and repay the loan.

Overall, Zenka is good app that you can take loan from owing to the time period you are given to repay back. Also, the peace of mind one get while using the app is worth.

And thats it on Loan apps.

Conclusion

Loan apps are here with us to stay. It’s up to you as a user to practice discipline when borrowing. Sadly, once you take a loan, you can only run away from it but you cannot hide.

On the other hand, digital lenders have many loopholes they need to seal.

With more negative reviews and flagging of the loan apps on googleplay, their services will risk suspension and the people who had borrowed money from them will be left celebrating they luck.

Also, Central Bank of Kenya and Office of the Data Protection Commission is on their case in a bid to regulate them.

Every digital lender therefore need to listen to the customer feedback and do as the customer request. Customer is the king here. For them to buy from you, respect and dignity has to be upheld.

As I close, if you need help with video production services, you can request a quote on www.techtubestudio.com.

Until next time bye bye and take care.